THE PRACTICAL POLITICS OF

Revenue in Bangladesh (prototype)

Author: Peter J Evans

Product No: Prototype

Date: October 2025

Download PDF

Table of contents

- Summary insights

- Summary propositions

- What is the problem?

- Who are the players?

- What are the rules of the game?

- The resulting state of play

- Propositions

- Further reading

- Endnotes

About the author

Summary insights

Bangladesh’s revenue problems go deeper than the current hole in public finances: the low tax-to-GDP ratio (7–9%) also undermines state capacity and social services.

Heavy reliance on value-added tax (VAT) burdens the poor. At the same time, Bangladesh’s elites have evaded taxes through exemptions and weak enforcement in prestige sectors.

Bangladesh’s ‘elite bargain’ (the unspoken deal that determines the allocation of power and resources in a country) has allowed elites to evade taxes with impunity and to use the revenue system as an engine for looting, illicit financial flows, and policy capture. This undermines the ‘social contract’: since citizens don’t trust the state to use their taxes well, they are reluctant to pay and depend instead on political patronage.

The National Board of Revenue (NBR) is inefficient, has outdated systems, and has been politicised and systemically corrupt. This has further enabled the ruling elite, business leaders, and bureaucrats to benefit from collusion, tax evasion, and exemptions.

Formal rules are overshadowed by informal practices, such as favouritism and discretion, including through the overuse of Statutory Regulatory Orders (SROs).

Decades of external technocratic tax reform programmes have been low ambition, have avoided more challenging political reforms, and had limited impact because they have been undermined by those with a strong interest in maintaining the status quo.

Summary propositions

There is a need to instigate politically informed, evidence-based, and economically rational policy and practice in Bangladesh in regard to revenue, including transformational reform that balances the urgent need for revenue generation with long-term system change to shift Bangladesh’s elite bargain.

We have six propositions, based on practical politically-informed thinking:

- Explicitly depoliticise the tax administration

- Measurably reduce corruption and loss within the revenue system

- Expand the tax base, but with care and nuance

- Ensure all technology and capacity building have political grounding and involve ‘culturisation’

- Build public trust as a priority, not an afterthought

- Ensure donors (all external partners) do better

We all – national reformers and international friends of Bangladesh – will have failed to learn from past mistakes if we continue to use technical tools to try to solve political economy problems.

I) WHAT IS THE PROBLEM?

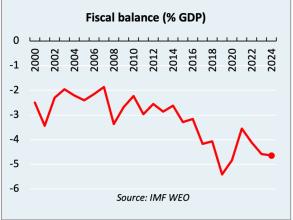

Bangladesh’s revenue system (collecting income through tax, customs and other sources) bumps along the bottom on most measures: social contract and tax morale, equality, tax-to-GDP ratio, and institutional shape. The problems are both economic (too little revenue is collected) and political (the revenue system is an engine for political capture, looting with impunity, and illicit financial flows). Due to these problems, over the last twenty years and more, revenue has increasingly fallen short of expenditure, resulting in rising fiscal overspend and unsustainable debt growth. Moreover, if GDP growth over this period has actually been overstated, this means the structural fiscal shortfall may have been even more severe.

Bangladesh’s malfunctioning revenue system undermines democracy and citizens’ trust and sense of having a stake in their country. These problems are deeply rooted in structural inefficiencies, systemic corruption, and particularly the politicisation of tax policy and administration.

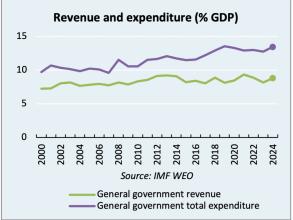

Bangladesh's tax-to-GDP ratio remains among the lowest globally, hovering between 7% and 9%[1],[2]. Government failure to generate sufficient domestic revenue leaves the country dependent on borrowing and international aid to finance fiscal deficits. The weak revenue base also constrains state investment in critical infrastructure, social services, and poverty alleviation, which in turn undermines long-term growth, prosperity, and equality[3].

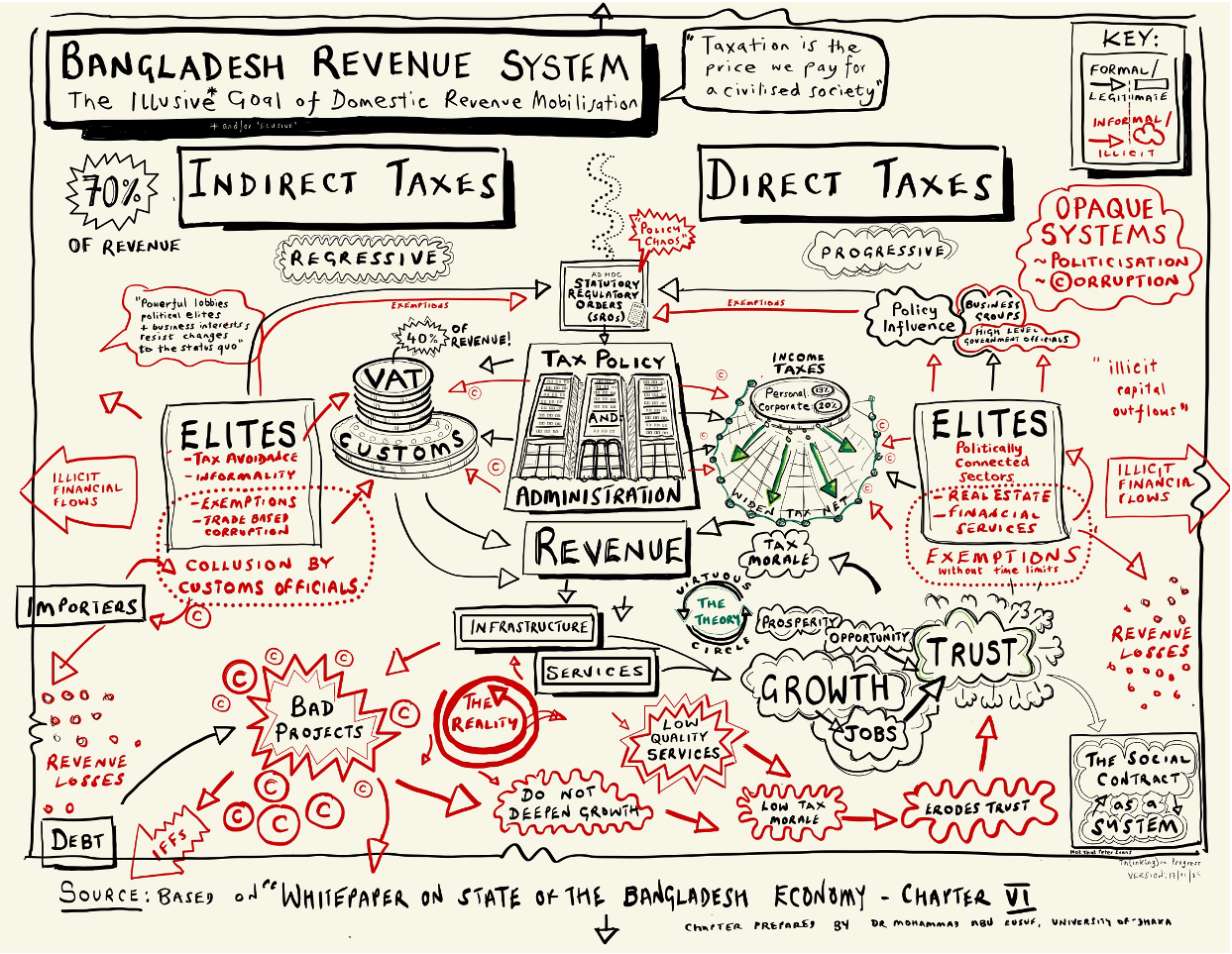

The revenue system is regressive, with indirect taxes doing the heavy lifting. Reliance on value-added tax (VAT) – accounting for 40% of revenue – disproportionately burdens the poor. Meanwhile, Bangladesh’s elites often avoid paying taxes. Direct taxes, including corporate and personal income taxes, contribute less than 30% of revenue, due to widespread tax evasion[4], exemptions, underreporting, and weak enforcement.

The informal economy constitutes more than 40% of GDP and is largely untaxed. Sectors with strong connections with ruling parties (real estate, energy, and financial services) benefit from generous exemptions and lax oversight. These sectors were also important in the systemic corruption, policy capture, and illicit financial flows that characterised the last decade of the Awami League government.

The National Board of Revenue (NBR) has chronic inefficiencies, outdated systems, and limited technology. These capacity constraints are compounded by active corruption and weak enforcement, allowing businesses and individuals to evade tax with impunity.

Public distrust in government discourages tax compliance, as citizens perceive tax revenues to be misused or siphoned off. Tax morale is low[5], creating a vicious cycle of low revenue collection, inadequate public investment, and persistent inequality, leading to further undermining of trust.

In theory, the state is tasked with providing public goods, in return for which citizens willingly cede some liberty and taxes to the state[6] (‘Paying tax is the glue in the social contract’[7].). However, in Bangladesh’s history, a weak social contract has resulted in an alternative model: winner-takes-all electoral politics, politicisation of the bureaucracy, and corruption. This makes it rational for citizens to rely on patronage networks, rather than to trust the state and to pay taxes.

Bangladesh’s reliance on external and domestic finance[8] further exacerbates the under-development of the social contract and elite capture of the revenue system.

II) WHO ARE THE PLAYERS?

Bangladesh’s revenue system is shaped by powerful groups, each of which has a stake in maintaining the status quo for their own self-interest. In this ‘elite bargain’ the most influential players have been the ruling political party, their allied bureaucrats and business leaders, and segments of the middle class. The revenue system was captured to serve relatively narrow elites at the expense of the majority. This elite bargain has dominated Bangladesh for decades. While this political equilibrium collapsed when looting of the state (and violence in defence of it) became too extreme and precipitated the ‘Monsoon Revolution’ of 2024, this type of elite bargain has survived previous transitions of political power and therefore may continue.

In Bangladesh, the political elite wields control of the state. It includes the core leaders of the ruling party and their patronage networks in government, business, and society at large. Successive governments, both under the Awami League and the Bangladesh Nationalist Party, have used tax policies and administrative systems to serve their own interests and consolidate their power[9]. Politicians rely on a network of patronage, granting tax exemptions and other favours to influential supporters, including business leaders and financiers, in exchange for political loyalty and party donations, and personal kickbacks. This symbiotic relationship reinforces corruption and weakens the enforcement of tax laws.

Within the bureaucracy, senior officials of the NBR and other bodies (Ministry of Finance, Customs etc) are another powerful group. The NBR is unusual as it is responsible for both tax policy and tax administration – functions typically separated in other fiscal systems. The NBR’s Chairman is a generalist civil servant appointed from Bangladesh’s elite ‘admin cadre’, while NBR staff are generally revenue specialists from the tax cadre. NBR Board members are from the tax cadre, which limits their career trajectories (a reality across Bangladesh’s second tier ‘non-admin’ cadres and a source of grievance). A high turnover of NBR Board members limits policy consistency.

The internal structure of the NBR is siloed, with a lack of integration and cooperation between income tax, customs, and VAT departments. The NBR has 3,500 officials and 10,000 supporting staff. Some of these officials benefit personally from the inefficiencies and opacity of the tax system, exploiting discretionary powers for ‘rent-seeking’ (unearned wealth). Corruption within the tax administration is reported (credibly) to be systemic, with tax officials colluding with taxpayers to underreport income, manipulate customs valuations, and circumvent audits.

The business community, particularly large corporations and politically connected groups in sectors like real estate, finance, and manufacturing, wield significant influence over tax policy. Through lobbying and political connections, they secure tax breaks, subsidies, and favourable treatment from regulators. Small and medium-sized enterprises (SMEs) often operate informally to avoid taxes altogether, perpetuating a culture of evasion.

International agencies, such as multilateral banks and bilateral donors, may regard themselves as neutral observers but in fact they are active players in the political economy of Bangladesh’s revenue system. Arguably, they continue to bring technical tools to a political game, and thereby perpetuate dysfunction. For example, they may focus narrowly on revenue yields and reforms such as digitisation, which may be actively undermined by vested interests in revenue administration and their political patrons.

Bangladesh’s middle classes also play a role in the revenue system, albeit relatively passively. Many resist paying taxes, justified by their distrust in government spending, frustration with opaque tax systems, and the burdensome nature of tax compliance. This resistance is both a cause and a consequence of broader governance and political failures.

III) WHAT ARE THE RULES OF THE GAME?

Formal rules and structures relating to revenue are set out in laws, regulations, and institutional frameworks, including the Income Tax Ordinance, VAT Act, and customs regulations. These establish the legal basis for tax collection and enforcement, and penalties for non-compliance. The NBR is responsible for administering these laws, overseeing direct and indirect taxes, and ensuring compliance.

The formal rules are overshadowed by informal rules, which govern how the revenue system actually operates in practice. At the heart of these informal rules is the politicisation of tax policy and administration. As noted above, successive governments have used tax as a tool for self-enrichment, and for rewarding allies and punishing opponents. Tax exemptions, selective audits, and discretionary enforcement are common, reflecting the influence of political interest over economic rationality.

Discretion also shapes the development and adoption of new formal rules. Business groups, politicians, and officials often collude to bend policy in their favour, particularly through excessive use of Statutory Regulatory Orders (SROs). SROs are administrative instruments used to modify tax laws, grant exemptions, or introduce measures without requiring legislative approval. SROs are typically directives of the Ministry of Finance, and are often influenced by business groups and senior officials. Their excessive use has become a tool for distributing political favours, with the energy sector offering some particularly egregious examples[10]. SROs undermine transparency and predictability, distort trade, massively reduce revenue, and contribute to general ‘policy chaos’. SROs constitute ‘policy capture[11]’ and arguably ‘state capture[12]’, when, in the interests of elite groups, they make legal what was previously illegal. SROs typically have no time limit (no ‘sunset clause’), therefore exemptions are perpetual.

Corruption distorts application of the formal rules. Tax officials often solicit bribes[13] in exchange for favourable treatment, such as reducing tax liabilities or ignoring irregularities. This creates a parallel system where compliance is determined not by adherence to the law, but by the ability to navigate informal networks of influence and payoffs. Businesses and individuals who can afford to engage in these practices are effectively exempted from the full weight of the tax system. Those who cannot, or will not, end up bearing the brunt of enforcement.

In regard to efforts to reform the revenue system, powerful elites and politically connected individuals resist any reforms (e.g. transparency measures) that threaten their ability to exploit manual processes for purposes of tax evasion, exemption, and corruption. At the same time, successive governments have prioritised short-term political gains over long-term reforms. Digitisation reforms provide one example. These are seen as politically risky by elites, as digitation could help expose systemic corruption, inefficiencies, and high-profile tax evasion. For this reason, policymakers are reluctant to fully embrace digital transformation. In addition, institutional entrenchment within the revenue agencies creates resistance to reform. Politically appointed officials fear losing the discretionary power and illegal income streams associated with manual systems.

Another informal rule is the widespread acceptance of tax evasion as a norm. Both businesses and individuals view underreporting income or avoiding taxes as a rational response to an inefficient and corrupt system. This culture of non-compliance is reinforced by weak enforcement mechanisms, which fail to hold violators accountable.

IV) THE STATE OF PLAY

The consequences of the elite bargain and the rules of the game described in the preceding sections are a revenue system that persists in a state that has been described as ‘policy chaos[14]’: not evidence-based and often economically irrational. Revenue administration is sclerotic and captured. However, the revenue system does have a logic, in terms of serving elite interests. While capacity is undoubtedly weak, a focus on capacity issues has been used to obscure the political drivers of poor performance: politicisation and capture, corruption, and protection of discretion and the status quo.

The term ‘revenue system’ is often regarded as referring to the narrow set of functions relating to raising taxes. However, this system also includes a set of component sub-systems (VAT, customs etc) and is also integrated into a range of wider complex systems – including balance of payments, trade, growth, and citizen–state relations. These interconnections mean that Bangladesh’s revenue problems have far-reaching consequences for the economy, governance, politics, and the country’s social fabric and stability. One of the most immediate impacts is the government’s inability to fund essential public services and infrastructure. With a limited revenue base, fiscal deficits persist, forcing the state to rely on borrowing to meet its obligations. This increases debt servicing costs, thereby crowding out resources that could otherwise be used for development.

Short-term action to reform the revenue system in Bangladesh will almost certainly focus on increasing VAT. This is a straightforward ‘lever’ and can yield a predictable increase in revenue. However, doing this will exacerbate the already regressive tax system, and thus inequality, but it will do little to address elite capture. It therefore also risks further eroding confidence in government and fuelling a sense of injustice and social discontent, particularly among middle- and lower-income groups, who already feel that the system is rigged against them. This would further undermine the social contract and would make it less likely that Bangladesh’s political system will break out of its ‘winner-takes-all’ cycle. It could also undermine Bangladesh’s long-term stability.

V) OUR PROPOSITIONS

Bangladesh’s revenue problems are extreme, despite decades of technical reform by national actors, supported by expertise and funding from international partners. This should be a warning against any return to technocratic business as usual: external support that continues to be technocratic, and to ignore history and context, risks complicity in future recapture. After the Monsoon Revolution, the reality of corruption, politicisation, and capture is ‘out in the open’, and there is now a rare opportunity to apply a different type of strategy.

Any revenue reform strategy – and the actions within it – should explicitly consider both political and technical dimensions and reflect the complex system in which revenue exists[15]. This includes actively tackling the negative system loops that sustain political capture and impunity, inequality, and tax evasion, while nurturing the positive loops, such as a progressive shift towards direct taxes, and building trust, tax morale, and a stronger social contract. This requires balancing short-term actions – to urgently fill the existing revenue gap – with a long-term strategy for achieving positive system outcomes[16]. Short-termism at the expense of system change is highly unlikely to shift the equilibrium away from the current elite capture.

It is important to recognise that political and business elites will continue to wield considerable influence over revenue policy and administration even if reform succeeds (the ‘future elite bargain’). Still, the aim of any reform should be to constrain this influence and to nurture ‘win-wins’ in growth, revenue, service delivery, social contract, and politics that are positively reinforcing and that benefit citizens and elites alike. In this context, while egregious corruption must be investigated and punished, Bangladesh will continue to need its current stock of revenue officials (provided they change their behaviour from hereon in): the NBR cannot punish its way forward.

Decades of institutional degradation has meant that institutions such as the NBR suffer from low capacity. This cannot tackled through increasing autonomy.

The long-mooted separation of tax policy from administration was the subject of the Revenue Policy and Revenue Management Ordinance, 2025. But without the NBR officials on their side, the Interim Government backtracked. The amended ordinance placated NBR staff by mandating that the RMD be led by revenue officials, while leaving the RPD open to macroeconomic and trade policy experts. This perpetuated the discretionary powers the reform sought to dismantle.

Our six propositions address systemic political constraints that hinder revenue mobilisation, and they also consider the wider benefits that revenue should help deliver for Bangladesh.

1. Explicitly depoliticise the tax administration

This process needs to start before technical reform is implemented. A first step must be a general, public recognition of the pervasiveness of politicisation of tax administration, the damage it causes, and a commitment not to let it take hold again after the recent Monsoon Revolution, regardless of which government is in power. Actions should include insulating the NBR from political interference and ensuring that appointments, audits, and enforcement decisions are based on merit, not patronage. This necessitates a problem-driven approach, actively considering how capture happens and testing methods to tackle this, rather than merely importing technical ‘solutions’ from other contexts. The international experience of ‘pockets of effectiveness[17]’, where state functions are protected, may be relevant to this effort.

Depoliticising tax administration will need to begin with an explicit political commitment – made publicly so that the government can be held to account. The July Charter was a set of political commitments that the BNP signed up to and indicates a consensus around institutional reform, but not specific technical reforms in tax administration. However, it could be a cogent issue for civil society to mobilise around.

2. Measurably reduce corruption and loss within the revenue system

In theory, this can be assisted by automating and simplifying key processes, such as tax filings, audits, and assessments, to minimise discretionary decision-making and opportunities for rent-seeking by tax officials cutting informal deals with taxpayers. Strengthening internal accountability mechanisms and imposing stricter penalties for corruption are also important. However, technical measures need to be constantly informed by political economy and risk analysis, as elites and ‘bad apples’ in tax administration will rapidly collude and develop strategies to again avoid tax, both legally and illicitly. Anti-corruption is a whack-a-mole[18] operation: you need to keep hitting corruption cases, as well as working hard to prevent them.

3. Expand the tax base, but with care and nuance

It is important to integrate the informal economy into the formal net through simplified registration processes and incentives for compliance, but this should be done realistically. Many informal businesses operate well below any likely threshold for taxation, and support the livelihoods of large numbers of poor people. Many who fall within the tax net do not file returns, both for legitimate reasons (businesses have folded but are still listed and should be removed) and bad (tax avoidance).

Targeting untapped ‘premium’ sectors, such as real estate, luxury goods, and digital business, will increase direct tax contributions and help tackle the overbearing political influence, impunity, and criminality of elites in these sectors. While one option is the ‘Al Capone[19] approach’ (by focusing on tax, you bring to light evidence that can help in tackling other criminality and impunity), it is also worth trying positive persuasion. Tax research and high net worth individual (HNWI) units have delivered results in other challenging political contexts[20], though the ability to do so in Bangladesh will depend on the nature of the country’s future elite bargain, including whether the richest citizens will pay their dues.

4. Ensure all technology and capacity building have political grounding and involve 'culturisation'

Investing in technology and capacity building can help modernise revenue systems. Digital tools, such as e-filing platforms and centralised databases, can improve efficiency and transparency. Training programmes for tax officials can enhance their ability to enforce compliance and serve taxpayers effectively. However, each depends on political intent and can be directly undermined by those who act to protect vested interests. For example, digitisation is unlikely to work in isolation but is more likely to work within a broader push to build a new culture (and to reshape the ‘elite bargain’) in the NBR and wider system.

It is important to consider the history of under achievement and disappointment, including in externally funded programmes. For example, vested interests directly undermined digitisation, yet this became a political flagship for the Awami League’s hollow promotion of state modernisation. Arguably, the international organisations that supported the digitisation programme were complicit in this illusion of modernisation. There are also allegations of irregularities in procurement[21].

5. Build public trust as a priority, not as an afterthought

Building trust is important but is difficult and slow. Citizens need to see tangible benefits from their tax contributions in order to feel motivated to comply with tax laws. The new government will need to engage the tax bureaucracy, not alienate it and bring in tax professionals and civil society as part of the process of reform. Transparency in government spending, coupled with public awareness campaigns, can help build a culture of trust and accountability. Communication should be evidence-based: there is a growing body of tax research that rigorously tests communication – individual and public –and measures its effects on subjects ranging from trust and tax morale to the actual quantity of revenue that is collected.

6. Ensure donors (all external partners) do better

International partners can play a role by supporting capacity-building initiatives and encouraging reforms. However, politically naïve technical approaches of the kind that have been all too common up to now risk actively doing harm.

External partners can help shore up Bangladesh’s economy that is currently precariously placed. The World Bank has a policy-based loan worth $500 million that will offer Bangladesh fiscal breathing space. In combination with the IMF programme, it can create room for a dialogue on governance reforms. But concrete revenue reform will not come about without domestic ownership and commitment.

Technical experts and tools cannot solve political problems. It will take courage, but politics should be permanently on the tax policy table. Regular, open-source, plain-language political economy analysis and research – such as annual updates of this paper (which could include, in future, implementation monitoring of major revenue reform initiatives and programmes) – would help make this effective and routine.

Further reading

For those wanting to read more we suggest the following key texts:

Eusuf, M. A. (2024) “The Illusive Goal of Domestic Revenue Mobilisation”. Chapter VI in: Bhattacharya, D. et al. (2024) “White paper on state of the Bangladesh economy – dissection of a development narrative”, Government of Bangladesh, draft, November.

International Growth Centre (2023) “Why does Bangladesh tax so little?”, IGC Blog, 3 April 2022. https://www.theigc.org/blogs/taxing-effectively/why-does-bangladesh-tax-so-little

Hassan, M. and Prichard, W. (2013) “The Political Economy of Tax Reform in Bangladesh: Political Settlements, Informal Institutions and the Negotiation of Reform”, International Centre for Taxation and Development (ICTD) Working Paper 14. https://www.ictd.ac/publication/the-political-economy-of-tax-reform-in-bangladesh-political-settlements-informal-institutions-and-the-negotiation-of-reform/

For deeper background of the analysis and ideas underpinning this note we have included detailed end notes as well as references.

Endnotes

Bangladesh’s GDP was inflated by the Awami League government. If GDP is recalculated and reduced, the tax-to-GDP ratio would look better but gross debt as a percentage of GDP would be worse. ↩

This data, and other analysis summarised in this paper, is drawn from the revenue chapter of Bhattacharya, D. et al. (2024) “White paper on state of the Bangladesh economy – dissection of a development narrative”, Government of Bangladesh, draft, November. ↩

The poor quality of public expenditure – planning, implementation, corruption in public procurement and contract delivery, and low-quality services – is as important a constraint as low revenue flow. ↩

See for example Financial Express (2022) “Many Bangladesh companies skip 'costly' tax compliance”, Financial Express, 02 January. https://thefinancialexpress.com.bd/trade/many-bangladesh-companies-skip-costly-tax-compliance-1641089763#google_vignette ↩

International Growth Centre (2023) “Why does Bangladesh tax so little?”, IGC Blog, 03 April 2022. https://www.theigc.org/blogs/taxing-effectively/why-does-bangladesh-tax-so-little ↩

Rousseau, J-J. (1762). The Social Contract (originally published as On the Social Contract; or, Principles of Political Right (French: Du contrat social; ou, Principes du droit politique). ↩

Cobham, A. (2022) “Paying tax is the glue in the social contract. When people pay tax, they are empowered to hold their governments to account for how their money is spent”. https://www.imf.org/en/Publications/fandd/issues/2022/03/Taxing-for-a-n…; ↩

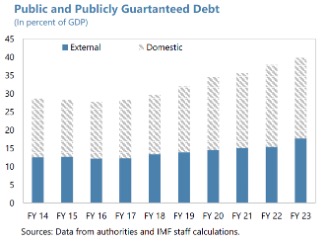

Bangladesh’s debt is more domestic than external:

Image

It is important to note how well-established this elite bargain is. For example, the following 2013 paper is still remarkably accurate: Hassan, M. and Prichard, W. (2013) “The Political Economy of Tax Reform in Bangladesh: Political Settlements, Informal Institutions and the Negotiation of Reform”, International Centre for Taxation and Development (ICTD) Working Paper 14. https://www.ictd.ac/publication/the-political-economy-of-tax-reform-in-bangladesh-political-settlements-informal-institutions-and-the-negotiation-of-reform/ ↩

The white paper states: ‘The excessive use of SROs has become a tool for distributing political favours, undermining the effectiveness of Bangladesh's tax policies. Although not exhaustive, Table 6.1 provides a brief overview of granted to selected large conglomerates.’ These include SROs granted in the energy sector to Summit Group and S.Alam Group. Summit Group is alleged to have leveraged its close ties with the Awami League government to maintain a dominant grip over Bangladesh’s power and energy sector, reshaping it to its advantage. (https://businesspostbd.com/national/aziz-khan-the-power-kingpin-under-hasinas-reign). S.Alam group is reported to be under investigation for a range of financial crimes and for money laundering. (https://www.straitstimes.com/singapore/courts-crime/bangladesh-probes-sporean-tycoon-for-financial-crimes-his-lawyers-call-it-a-smear-campaign). ↩

‘Policy capture’ means that public decisions over policies are consistently or repeatedly directed away from the public interest towards a specific interest. See for example OECD (2017) “Preventing Policy Capture: Integrity in Public Decision Making”. https://www.oecd.org/en/publications/2017/03/preventing-policy-capture_g1g78280.html ↩

For a definition of ‘state capture’ see for example Dávid-Barrett, E. (2023) “State capture and development: a conceptual framework”, J Int Relat Dev 26, 224–244. https://doi.org/10.1057/s41268-023-00290-6. https://link.springer.com/article/10.1057/s41268-023-00290-6 ↩

In a survey by the Centre for Policy Dialogue, 45% of private companies surveyed stated that they were asked for a bribe by tax officials in financial year 2023. See CPD (2025) “Corporate Income Tax Reform for Graduating Bangladesh: The Justice Perspective”. https://cpd.org.bd/resources/2025/04/Presentation-on-Corporate-Income-Tax-Reform-for-Graduating-Bangladesh.pdf ↩

Bhattacharya, D. et al. (2024 “White paper on state of the Bangladesh economy – dissection of a development narrative”, Government of Bangladesh, draft, November 2024. p. 88. ↩

See Evans, P. (2025) “Picture this 3: Bangladesh Revenue System”. https://notthatpeterevans.substack.com/p/picture-this-3-bangladesh-revenue?r=1x9c6h

Image

Increasing VAT is very attractive because it is a clear and known policy lever that can generate a predictable amount of additional revenue. VAT is already collected, and we know from whom, so we can predict what will happen with an increase in the rate or the application of VAT to a wider range of goods and services. In contrast, broadening the tax base is much more complex and difficult, and will encounter a new set of structural and political economy challenges that will need to be navigated through policy and in implementation. However, both approaches are important, and the former cannot be applied at the expense of the latter. ↩

‘Pockets of effectiveness are public organisations that function effectively in providing public goods and services, despite operating in an environment where effective public service delivery is not the norm. History suggests that pockets of effectiveness have proved critical to developmental state success in the global south’. See https://www.effective-states.org/pockets-of-effectiveness/ ↩

In the arcade game Whac-A-Mole the player quickly and repeatedly hits the heads of mechanical moles with a mallet as they pop up from holes. For use of the term in relation to anti-corruption strategy see David-Barrett, E. (2020) “Anti-corruption in Aid-funded Procurement: Whacking the Mole is Not Enough”. https://giace.org/anti-corruption-in-aid-funded-procurement/ ↩

See https://prologue.blogs.archives.gov/2011/07/26/the-taxman-cometh-u-s-v-alphonse-capone/ ↩

See for example the case of Uganda: https://www.ictd.ac/news/bringing-uganda-s-rich-into-the-tax-net/ ↩